Private Equity Deal Activity Review & 2025 Outlook

A Modest Recovery in 2024 and Guarded Optimism in 2025

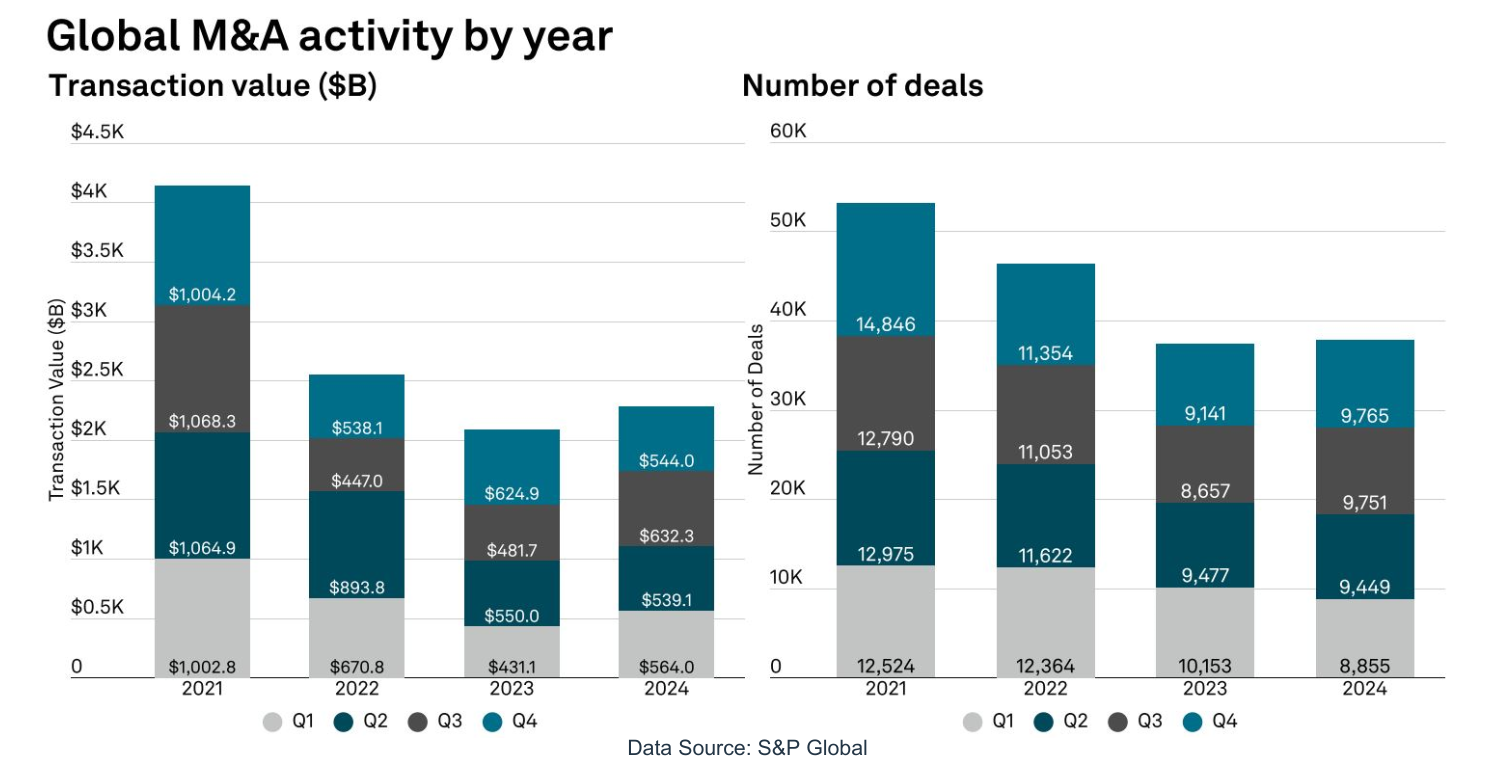

Despite initial expectations for a strong rebound in M&A activity driven by pent-up demand, private equity managers saw a slower recovery in 2024 than initially expected, with improvement in the latter half of the year.

This delay was largely due to macroeconomic challenges, including inflationary pressures, ongoing geopolitical instability in Ukraine, China and the Middle East, the U.S. presidential election and the complexities of managing existing portfolios that are larger than typically held by private equity funds given the subdued exit environment. However, deal activity ticked up globally in the second half of 2024, buoyed by easing interest rates in September, narrowing loan spreads and growing confidence in the resilience of the deal environment.

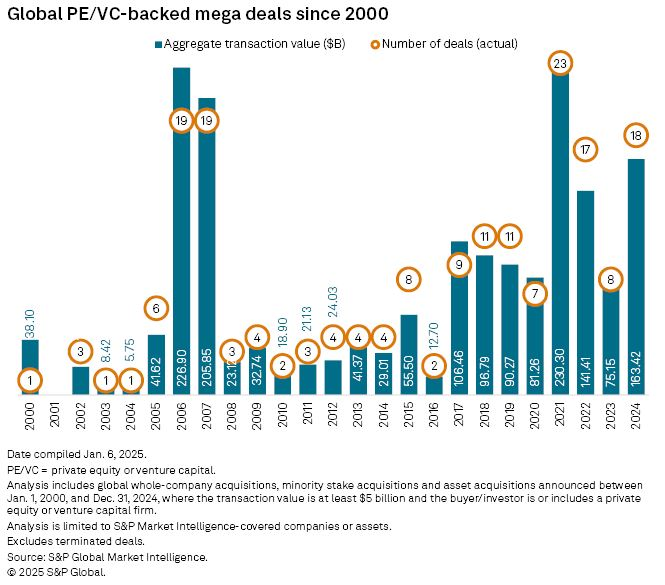

This was evident in particular for private equity and venture capital-backed mega deals valued at over $5 billion, which jumped by 25% in deal value compared to 2023. While global deal value rose compared to 2023 (mainly due to the increase in mega-deal value), deal count remained relatively flat.

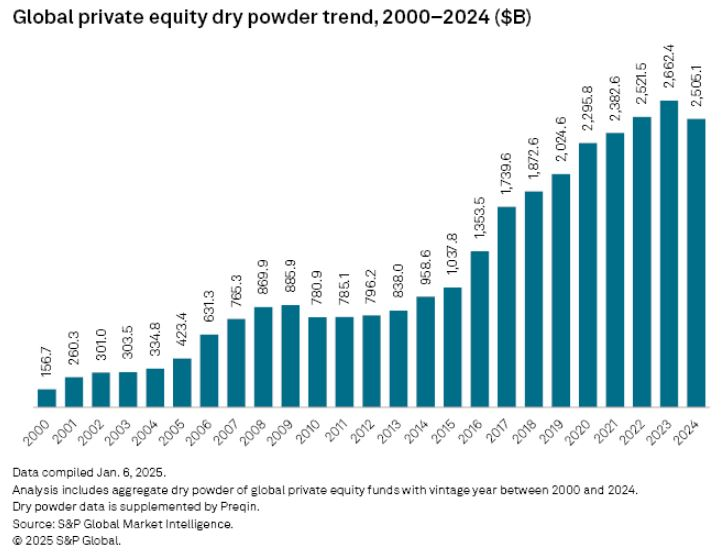

However, the middle market has remained resilient. Middle market buyout funds, whose strategies focus on companies valued at $1 billion or less, saw an increase in number of deals closed in 2024, with middle-market deals accounting for 95% of all M&A deal activity. There was also an increase in both the number of funds and capital raised by middle-market funds compared to 2023. At the same time, middle-market dry powder has declined, as dry powder is being deployed into middle-market deals.

A more active market is anticipated in 2025, given the high levels of dry powder. With increased pressure on private equity funds to invest their capital in 2024 (particularly as various funds approach the end of their investment cycles on the back of several years of subdued deal-making), we saw a 6% decrease by the end of 2024 in the amount of dry powder, compared to the record $2.66 trillion of dry powder available at the end of 2023.

We expect private equity funds to continue to respond to the pressures from their investors to put their capital to work. While this will likely lead to increased deal-making, sponsor-led exits and higher fundraising, challenges such as high borrowing costs, valuation gaps between buyers and sellers and the effects of certain executive orders, such as the imposition of tariffs, from the Trump administration may continue to limit acquisition activity.

Key Trends Expected for 2025

With Donald Trump back in the White House and rapidly implementing his policy agenda through executive orders, private equity funds must navigate both new opportunities and challenges amid significant changes in regulatory policy. In his first weeks in office, President Trump has issued a series of executive orders, including introducing and expanding certain tariffs. These trade measures could have wide-ranging effects on private equity portfolio companies and M&A deal flow, requiring private equity investors to reassess risk exposure and portfolio strategies. For real-time updates on the Trump administration’s executive orders and their impact, visit Akin’s Trump Executive Order Tracker.

Beyond U.S. trade policy, anticipated deregulation (particularly in the U.S.) and shifts in tax policy may significantly impact the market, requiring private equity funds to adapt quickly and strategically. Private equity funds will need to be agile in reassessing their strategies, capitalizing on emerging opportunities and managing the potential obstacles as these policy changes unfold.

With shifting regulatory priorities, private equity firms must prepare for a dynamic and fast-changing investment landscape in 2025 to effectively seize potential advantages and hedge against downside risk.

We see five key trends for 2025 in a fast-moving landscape:

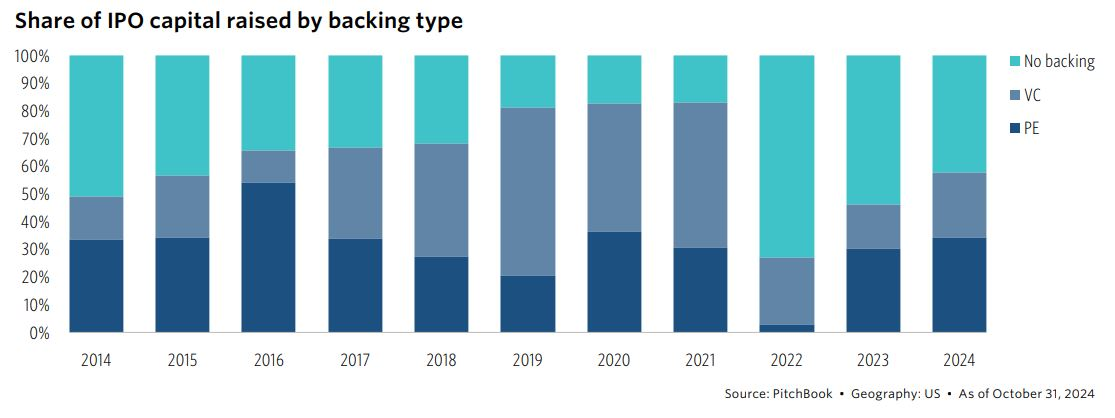

1. Tempered deal activity rebound. The positive momentum that began in the second half of 2024 is expected to continue in 2025, driven by a surge in mega deals, middle-market transactions and private equity-backed IPOs, and supported by market fundamentals of falling interest rates, high levels of dry powder in both private equity and private credit and strengthening fundraising. However, private equity funds are taking a more measured approach as they assess the macroeconomic impact of President Trump’s early executive orders. While optimism remains for increased trading of high-quality assets—as auctions become more competitive in all geographies, investor confidence grows in private-equity-backed IPOs and the logjam of overdue exits finally eases—these expectations are tempered by predictions and careful scrutiny of Trump’s regulatory actions and their potential market effects.

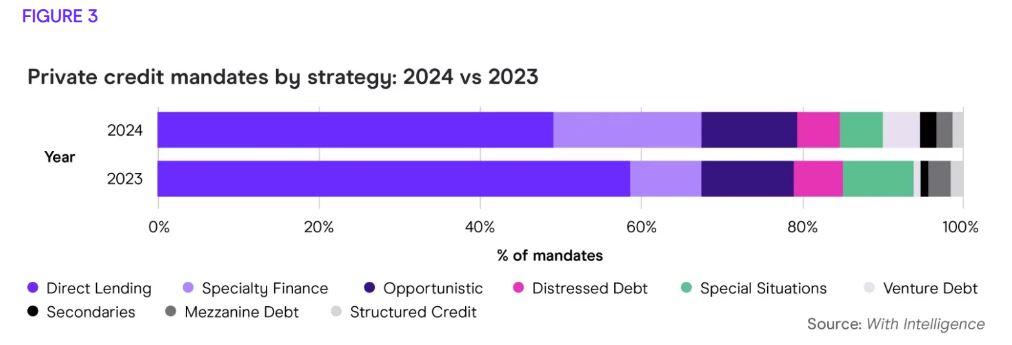

2. Credit flows more freely. While U.S. and European leveraged loan markets rebounded in 2024, the vast majority of market activity involved refinancings and recapitalizations. With balance sheets shored up and maturities pushed out, we expect private capital providers to lead the response to borrower demand to finance new deal flow. Private debt providers continue to expand quickly even with the rebound in credit market liquidity as they prove to be constructive partners in challenging situations and continue to offer flexible, competitive capital. Given these trends, we see no signs of private debt funding slowing in 2025. We also anticipate a continued increase in the deployment of creative capital solutions by private capital providers, including hybrid / preferred equity transactions.

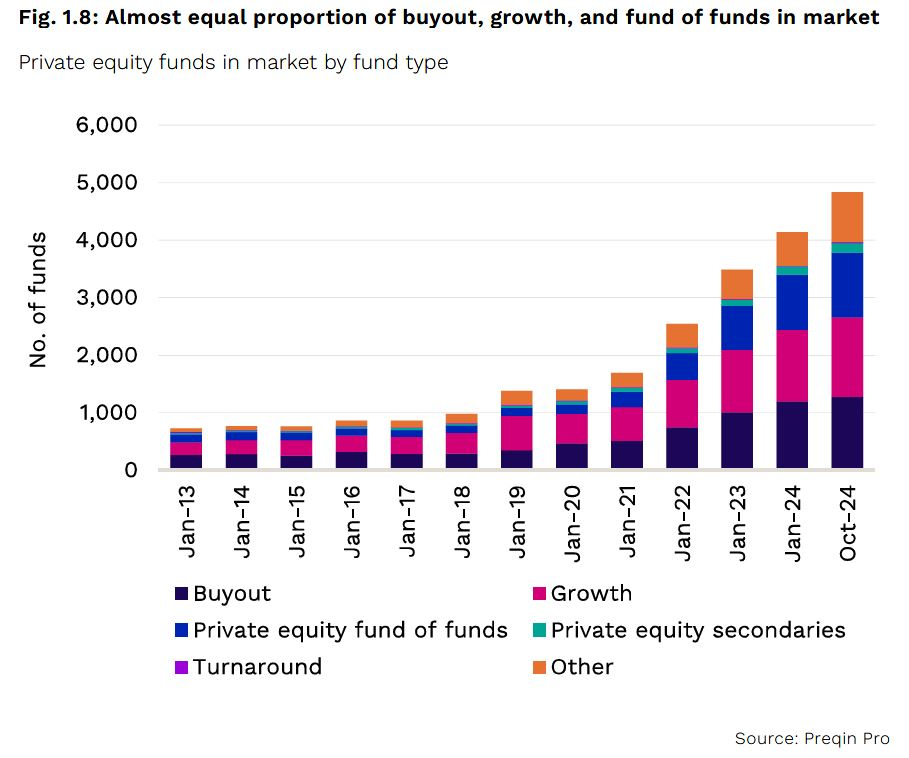

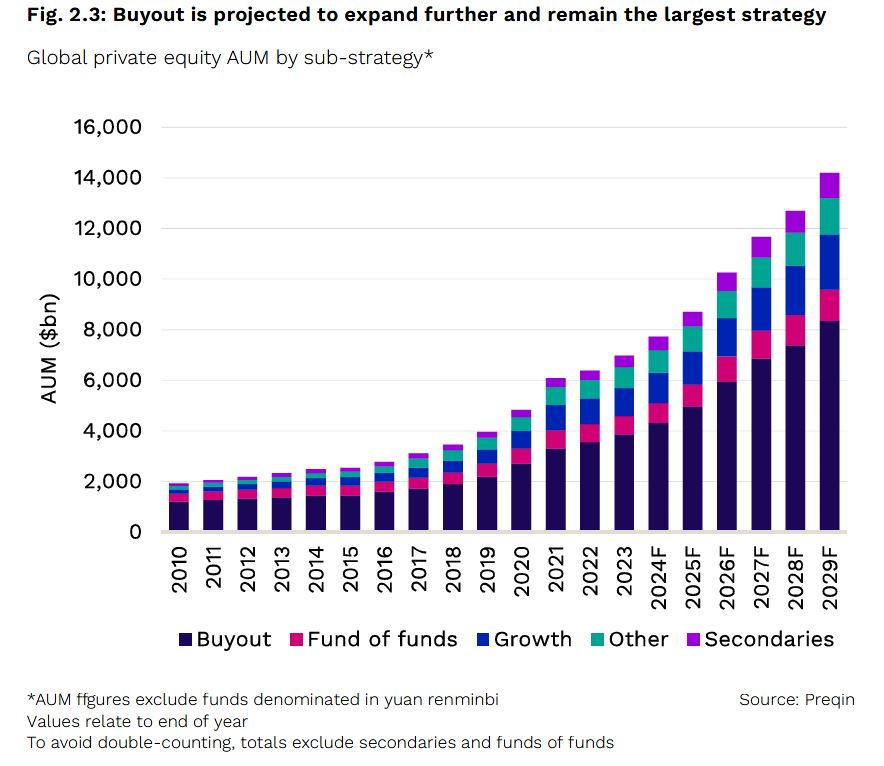

3. Funds benefit from looking beyond buyouts. Following a challenging period for buyout capital deployment, private equity funds enter 2025 in strong shape to address a broad array of market opportunities. We have seen sponsors increasingly diversifying into structured equity and minority stake transactions, solutions that have found favor with borrowers struggling to bridge gaps through a tight credit environment. We expect this trend to continue and even strengthen in 2025. As LBO shops have diversified into new strategies and asset classes through a period of GP consolidation, many are poised to reap the rewards as more deals enter the market.

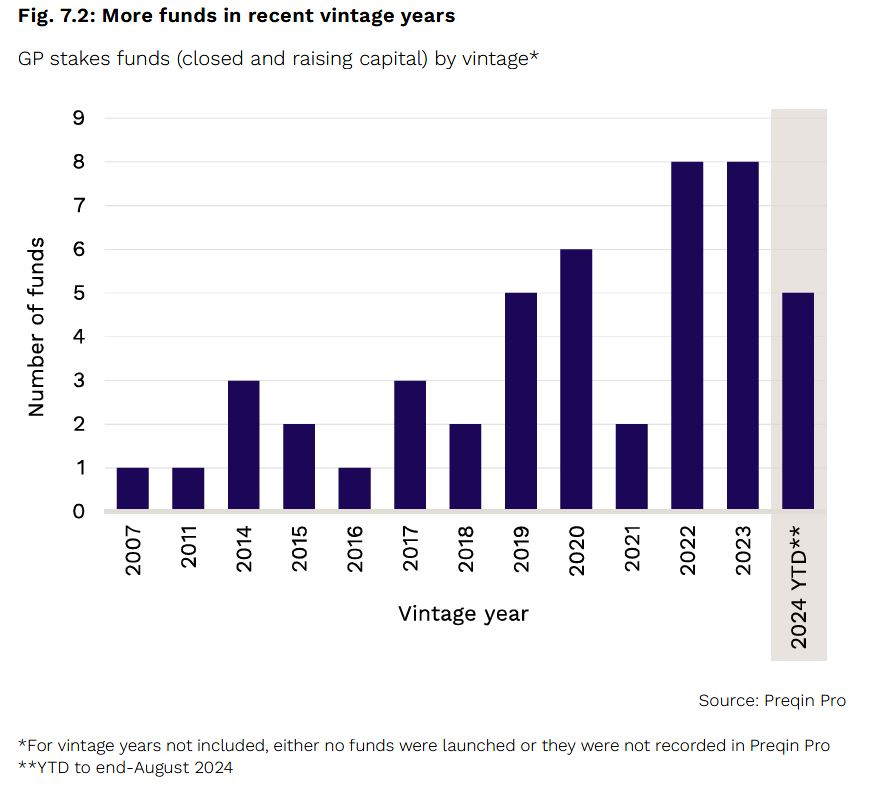

4. Fund liquidity increases. As the market rebounds, we also see funds taking advantage of an expanding roster of options as they seek to tap liquidity, extend hold periods and return capital to LPs. The secondaries market looks set to notch another record year when 2024 totals are tallied, buoyed by trading of LP portfolios as well as the continued uptake of GP-led solutions. With NAV financing, GP stake sales and the ongoing co-investment boom all growing in popularity, the range of options in the toolbox of sponsors seeking liquidity will continue to expand in the year ahead.

5. Transformation and opportunity in certain sectors. The shifting political backdrop in the U.S. and elsewhere comes at a crucial time for several sectors.

-

- AI and technology remained the headline focus for investors through 2024 and we expect that to remain the case, even as governments across the globe ramp up scrutiny in certain segments of the market and promises export controls and investment restrictions in the tech race with China.

- Energy and Infrastructure is set to feel the impact of a shifting political narrative, particularly in the U.S. where we expect to see the repeal of many of Biden’s edicts on net zero and the environment. While navigating regulatory change will present challenges, investor appetite is strengthening around the sector and deal opportunities abound across traditional energy, energy transition, utilities, digital, carve-outs and midstream consolidation.

- Health Care will be a focus for regulatory reform, especially in the U.S., as Trump looks to unwind Biden's policies, reform drug pricing, encourage innovation around AI and medical technology and prioritize domestically produced medicines. After a subdued period of deal flow, we look forward to more transactions in 2025 fueled by innovation and a growing appetite for technology and services deals.

- Financial Services is expected to see broader deregulation, with respect to the CFPB, crypto and AI, which may spur further investment in this space from private equity. Additionally, private equity investors with banking investments will need to grapple with Basel III Endgame requirements, which are set to take effect in mid-2025.

- Aerospace and Defense is expected to continue seeing increased private equity deal activity, consistent with 2024.

- Professional sports continue to grow as an asset class for private equity, driven by evolving ownership dynamics and growth fueled by media rights, international expansion and new revenue models.

- Food and agriculture is set to benefit from various government’s increased support of domestic production and deregulation to prioritize food productivity and affordability over emissions. We expect private equity to continue to get behind strategies targeting food security, technological innovation, and long-term sustainability.

Authors