Denial Is Futile—The Global Minimum Tax Is Coming. Will Implementation Impact Equity Valuations?

By: Stuart E. Leblang, Serena Lee, Matthew Durward-Thomas, Michael J. Kliegman and Amy S. Elliott

Even though U.S. lawmakers are not on the same page when it comes to the OECD’s global minimum tax regime1 (also referred to as Pillar Two or the Global anti-Base Erosion (GloBE) rules), many multinational corporations’ effective tax rates (ETRs) will increase as soon as 2024 due to initial implementation of a 15-percent global minimum tax in many major countries (see pages 8-9). The 15-percent minimum tax is imposed on a financial income/book base (with adjustments2) and is designed to ensure that a minimum level of tax is paid on the income arising in each jurisdiction in which an entity operates (minus a substance-based carve-out).3

Movement to change these countries’ laws over the last six months (plus promises by dozens of others, including the United States, to either follow suit or not get in the way—which, to be clear, is all that it means to be an Inclusive Framework signatory4) has created enough momentum to cause the Pillar Two train to pull out of the station. Now it looks like nothing will be able to stop its initial implementation—not foot-dragging by the United States, threats of retaliatory taxes by House Republicans (see more about this on page 10) nor warnings of treaty challenges by multinationals. Implementation will be labored and (despite best efforts by the OECD) not perfectly coordinated, and multinationals could face double taxation.

Has the Market Priced in Pillar Two? – Delayed Disclosure

A key question we wanted to explore is whether any publicly traded multinationals will have material cash-tax impacts and reduced earnings-per-share as a result of Pillar Two and, if so, which firms are most vulnerable? Unfortunately, that’s a hard question to answer due to a disclosure void that could theoretically produce unexpected market impacts in the coming months, as companies only disclose potential material impacts on a delayed basis, even though some companies may be in a position to ascertain the risk level now.

On May 23, 2023, the International Accounting Standards Board (IASB, which issues IFRS)5 announced temporary relief6 allowing companies affected by Pillar Two implementation to not disclose certain information about their exposure7 (not even a broad, estimated range of impact, let alone quantitative details of expected changes to average ETR8) until 2024 (which is when Pillar Two actually starts to go into effect in many countries). Then in 2024, if implementing legislation has been substantively enacted but the new tax is not yet effective (for example, Japan’s legislation goes into effect for tax years beginning on or after April 1, 2024), the disclosure could simply state that the company is still determining its exposure.9

The IFRS disclosure relief is an acknowledgement that multinationals are struggling to assess how Pillar Two will impact their worldwide operations and need more time to reliably make the calculations10 (and possibly plan to protect future cash flows) underlying the unsettled rules that will add a new level of complexity to interconnected but disparate international tax laws.

FASB, the body that generally regulates U.S. GAAP disclosures, announced11 that Pillar Two is considered an alternative minimum tax (which means that it won’t impact GAAP calculations of deferred tax assets and liabilities). However, FASB has not issued separate disclosure requirements concerning the impacts of GloBE taxes on reporting entities, despite the fact that on March 15, 2023, it circulated a proposed update to its income tax disclosure standards that would, among other things, require companies to disclose the amount of income taxes paid by jurisdiction each year12 as well as disclosures on the effects of new tax laws (among others).13

One firm is warning clients that “the calculations required by the Pillar Two model rules . . . depend on a number of factors that are difficult, if not impossible, to forecast reliably.”14 The takeaway is that investors may not get disclosures detailing the cash tax impacts of Pillar Two until the initial top-up tax actually takes effect in 2024—at which point companies may still be navigating restructuring decisions15 that could buy them time before Pillar Two’s most punitive tax (the UTPR or undertaxed profits rule) comes into effect in 2025—complicating investors’ capital allocation decisions.

The lack of disclosure concerning the risks that GloBE top-up taxes pose to public companies’ bottom lines is concerning.16 Rather than wait while companies continue to “monitor” developments and “evaluate” the potential impact on their operations, should investors simply assume that any large multinational with subsidiaries in low- or no-tax jurisdictions (especially pharma and tech multinationals that tend to have a lot of profits tied to intellectual property (IP) that would have presumably been booked in such jurisdictions) will end up paying more taxes as a result of Pillar Two? (Note that certain firms are able to model Pillar Two’s impact on companies—see, for example, PwC’s centralized calculation engine.)17

But, despite efforts by various regulators to increase corporate tax transparency by requiring country-by-country tax reporting,18 including an expression of support for such disaggregated tax reporting by Securities and Exchange Commission (SEC) Chair Gary Gensler19 (possibly influenced by calls from investors for such information to be made public20), few companies voluntarily disclose their tax planning details—even if their strategies aren’t considered aggressive. This makes it challenging for investors to sort out which multinationals will bear the brunt of the estimated $220 billion of increased corporate tax revenues adopting countries will be able to collect each year as a result of Pillar Two.21

Pillar Two Rules and Implementation

To understand when Pillar Two goes into effect, you first have to understand that there are actually four separate Pillar Two rules that work in conjunction to ensure that profit earned in a group is taxed at an effective rate of at least 15 percent (and note that not all taxes are counted when determining ETR for GloBE purposes22). Pillar Two generally only applies to any multinational group (including certain related entities)23 with annual consolidated group revenue of at least €750 million, which (depending on the day) is about US$820 million, in at least two of the preceding four years.24 It is estimated that some 8,000 multinationals will be in scope for Pillar Two.25 Once in scope, the four rules are:

- the income-inclusion rule (IIR), which many countries plan to implement in 2024;

- the qualified domestic minimum top-up tax26 (QDMTT), which is optional under GloBE;

- the undertaxed profits rule27 (UTPR), which many countries plan to implement in 2025;

- and the subject to tax rule28 (STTR), which we will not detail in this report.

Of these rules, the UTPR is arguably the most powerful, as it would essentially give countries that don’t currently have a right to tax another country’s income (under a top-down approach) the ability to do so if the primary taxing jurisdiction doesn’t impose tax at an effective rate of at least 15 percent. Even though the United States isn’t widely considered to be a low-tax jurisdiction (and even though the United States hasn’t adopted Pillar Two), implementation of Pillar Two rules by other countries could harm many U.S. multinationals, because taxes paid under either the Global Intangible Low-Taxed Income (GILTI) regime29 or the Corporate Alternative Minimum Tax (CAMT) regime30 are generally not considered fully covered taxes under the GloBE rules.31 Further, certain critical U.S. tax credits (namely the Section 41 research credit32) currently apply to reduce the effective rate of tax paid under the GloBE rules (increasing the Pillar Two risk to a U.S. multinational), whereas many tax incentives provided by other countries (structured as refundable tax credits or direct grants) don’t reduce GloBE ETR.33

The three primary GloBE rules apply as follows. If the source country (the country where the economic activity triggering the tax is located) doesn’t collect tax on book/GloBE income at an effective rate of at least 15 percent (either under the country’s normal corporate tax rules or by way of a QDMTT), then dibs for taxing the difference (the top-up) go first to the ultimate parent residence country (where the ultimate parent is headquartered/domiciled, which can impose the tax via IIR), second to the country where the intermediate-tier parent is domiciled (via IIR) and finally to the country where any other affiliated entity in the group is domiciled (via UTPR).

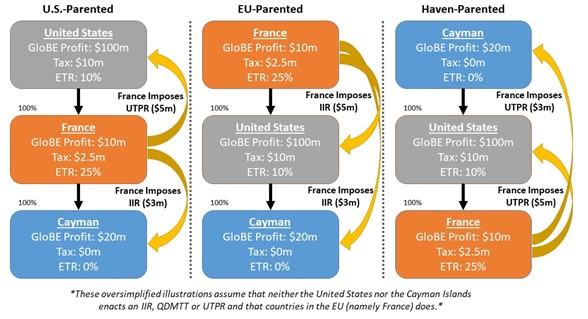

So, for example, consider a simplified fact pattern (see example illustration on page 5, at far left) of a U.S. parent company with a high-taxed French direct subsidiary and a low-taxed Cayman indirect subsidiary. If we assume that neither the United States nor the Cayman Islands enacts an IIR, QDMTT or UTPR—and we assume that France does—then (in 2024) France can collect a $3 million top-up tax (via IIR) on the undertaxed Cayman profit (assuming the profits and tax rates noted in the example, which are for illustrative purposes only). Further (in 2025), France can collect what amounts to a $5 million top-up tax (via UTPR) on the undertaxed U.S. profit (by effectively adjusting the tax liability of the French subsidiary34). Illustrative examples are also provided (middle and right) for EU-parented and tax haven-parented multinationals.

The upshot is that any multinational that has (somewhere in its group) undertaxed subsidiaries that are either themselves domiciled in (or are sitting below entities that are domiciled in) QDMTT/IIR-adopting countries (such as France or Ireland) could be subject to additional tax in 2024. This explains why some multinationals are considering moving their undertaxed subsidiaries—in non-QDMTT-adopting countries—out from under holding companies domiciled in IIR-adopting countries.35

At a high level, this initial impact could be worse for non-U.S. parented multinationals. Why? Because GILTI is treated as a blended controlled foreign corporation (CFC) tax regime for purposes of the GloBE calculations for a limited time (generally for tax years that begin before 2026). This essentially means that some portion of GILTI tax—determined by application of a mechanical formula—may be allocated to foreign low-tax jurisdictions, potentially reducing the amount of top-up tax imposed in respect of those jurisdictions by Pillar Two. Moreover, as U.S.-parented multinationals are already subject to potential top-up taxes on undertaxed foreign income under GILTI, the additional top-up tax potential could merely be incremental if GILTI tax is already being assessed with respect to the undertaxed income.

While GILTI may help to lessen the risk that IIRs and UTPRs pose to U.S. multinationals,36 without changes to the GILTI regime so that it qualifies as a Pillar Two compliant IIR, this relief will likely not extend beyond 2025 (except for fiscal year taxpayers, where relief could extend to a portion of 2026). Moreover, if the United States does not allow a credit for QDMTTs (which are assessed before GILTI), then the analysis significantly changes. Further, given the ability of U.S. multinationals to blend income from high-tax and low-tax foreign subsidiaries to lessen or altogether avoid the imposition of GILTI, even in respect of tax years beginning before 2026, the additional tax to a U.S. multinational could nevertheless be substantial in certain cases.

Assuming Pillar Two implementation proceeds on schedule, the impact will likely be more significant in 2025 when UTPRs go into effect. At that point, it no longer matters whether the entity domiciled in a UTPR-adopting country sits above an undertaxed entity. Any multinational that has an undertaxed entity in its group (including at the parent level) and also has even one entity domiciled in a UTPR-adopting country in its group (no matter the relationship between those two entities) could be subject to additional tax in 2025—limiting restructuring options.

This could be particularly problematic for U.S. multinationals that, under the GloBE rules, have an ETR below 15 percent (in part, because of U.S. tax incentives such as the research credit). The U.S. GAAP average tax rate for large, publicly-traded corporations was 11.3 percent for tax years 2019 and 2020, meaning that a significant percentage of large U.S. multinationals pay less than 15 percent on their income in the United States37 and may continue to do so even with the enactment of CAMT, which generally preserves the benefit of the research credit.

Additional clarification is needed to determine the extent to which some portion, if any, of CAMT—which may not qualify as a QDMTT—might factor into the GloBE calculation.38 Further, because GILTI is only treated as a blended CFC tax regime under the GloBE rules for a limited time, as soon as that transition relief ends (generally for tax years that begin in 2026), the added tax to U.S. multinationals as a result of such a sunset could be significant. As one observer recently put it, “The screws tighten each year.”39

Which Countries Are Implementing Pillar Two?

As far as the status of Pillar Two enactment goes, it varies by country and changes by the day (see the table on pages 8-9 identifying the Pillar Two implementation status of certain major countries—this is not a comprehensive list). According to the IRS, about 80 percent of U.S. multinationals’ total foreign profits before income tax were earned in 15 countries, at least nine of which plan to enact Pillar Two.40 A significant development was the December 14, 2022 agreement by European Union (EU) member states to implement Pillar Two (mandatory IIR in 2024 and UTPR in 2025, optional QDMTT), with member states being instructed to transpose the directive into national law by the end of 2023.41

|

COUNTRY |

IIR |

UTPR |

QDMTT |

Notes |

|

Australia42 |

2024 |

2025 |

2024 |

On May 9, 2023, Australia announced it will adopt legislation implementing Pillar Two (no draft yet). |

|

Bermuda43 |

-- |

-- |

-- |

On Feb. 17, 2023, the Ministry of Finance presented considerations about the impact of Pillar Two. |

|

Canada44 |

2024 |

2025 |

2024 |

On March 28, 2023, the Federal Budget was released. In a supplement to Budget 2023, the Canadian government indicated that it “intends to release draft legislative proposals for the IIR and domestic minimum top-up tax . . . in the coming months” effective for fiscal years on or after Dec. 31, 2023. No legislation yet on a UTPR. |

|

France45 |

2024 |

2025 |

Unclear |

Announced intention to implement (no draft yet). |

|

Germany46 |

2024 |

2025 |

2024 |

On March 20, 2023, the German Ministry of Finance published a discussion draft of Pillar Two legislation. |

|

Ireland47 |

2024 |

2025 |

2024 |

On March 31, 2023, Ireland said it intends to incorporate the EU Minimum Tax Directive into law via the October 2023 Finance Bill (no detailed legislative draft yet). |

|

Italy48 |

2024 |

2025 |

Unclear |

Announced intention to implement (no draft yet). |

|

Japan49 |

2024 |

Unclear |

Unclear |

LEGISLATION PASSED -- In late March 2023, Japan enacted an IIR that will apply to fiscal years beginning on or after April 1, 2024 (it has not yet passed legislation for a UTPR or a QDMTT). |

|

Netherlands50 |

2024 |

2025 |

2024 |

On May 31, 2023, legislation was introduced for debate and is expected to enter into force on Dec. 31, 2023. |

|

Singapore51 |

2025 |

2025 |

2025 |

On Feb. 14, 2023, Singapore’s budget detailed plans to implement the GloBE rules starting in 2023. |

|

South Korea52 |

2024 |

2024 |

Unclear |

LEGISLATION PASSED – At the end of Dec. 2022, South Korea enacted an IIR and a UTPR into law for fiscal years beginning in 2024. It may in the future enact a QDMTT. |

|

Spain53 |

2024 |

2025 |

Unclear |

Announced intention to implement (no draft yet). |

|

COUNTRY |

IIR |

UTPR |

QDMTT |

Notes |

|

Switzerland54 |

2024 |

2025 |

2024 |

On June 18, 2023, a constitutional amendment was adopted authorizing an implementing ordinance. The latest version of a draft ordinance is circulating and open for public consultation through September 2023. |

|

United Kingdom55 |

2024 |

2025 |

2024 |

Draft legislation to incorporate Pillar Two into U.K. law (Spring Finance Bill 2023), was released March 23, 2023. |

How to Determine Which Companies Will Be Hit? A Pillar Two Primer

With Pillar Two legislation only having actually been enacted in two countries so far (Japan and South Korea), very few public companies have disclosed in SEC filings a specific quantified risk of the impending global minimum tax rules. For example, on February 23, 2023, in its annual report, Xerox Holdings Corporation (NASDAQ: XRX) noted the adoption of Pillar Two by EU member states, but merely added that “as countries unilaterally amend their tax laws to adopt certain parts of the OECD guidelines, this may increase tax uncertainty and may adversely impact our income taxes.”56

In its quarterly report released May 5, 2023, Dolby Laboratories, Inc. (NYSE: DLB) also noted the EU development, adding that “individual countries have made and could make additional competing jurisdictional claims over the taxes owed on earnings of multinational companies in their respective countries or regions. To the extent these actions take place in the countries that we operate, it is possible that these law changes and efforts may increase uncertainty and have an adverse impact on our effective tax rates or operations.”57 Not super helpful.

The problem is that determining which companies would be most at risk if Pillar Two is broadly enacted is complex, because the GloBE rules are complex. If an entity is within scope, it should generally expect the IIR, QDMTT and UTPR to apply such that it will have an effective tax rate of at least 15 percent on its profits in every country in which it operates (generally regardless of whether that country has itself adopted Pillar Two).

However, the details are a bit more complicated. For example, just like the GILTI regime makes an effort to exempt income from tangible investments from the minimum tax (by allowing for a special deduction equal to 10 percent of the qualified business asset investment or QBAI), Pillar Two has a similar substance-based carve-out. While the rate is lower (at only 5 percent, although it starts out at either 10 percent or 8 percent and then is reduced over a period of 10 years58), the substance-based income exclusion includes a lot more (the carrying value of eligible tangible assets in the country plus eligible payroll costs in the country). This effectively means that in order to calculate the top-up tax, you take:

(15% – ETR) x (net GloBE income – substance-based income exclusion)

Note that the GloBE rules do not require that an adopting country change the corporate tax rate applied to its domestic entities (although it can choose to do so, including by way of a QDMTT)— just the top-up rate applied to income of their foreign subsidiaries. For example, if the United States were to adopt a Pillar Two IIR (or make GILTI compliant with Pillar Two59), then if a U.S. parent company has foreign operations in a country such as Ireland and those operations are only subject to a 12.5 percent effective tax rate (paid to Ireland, assuming Ireland doesn’t adopt a QDMTT, which it has indicated it will), the U.S. parent will owe a top-up tax of 2.5 percent (15 minus 12.5) on that foreign income to the U.S. Treasury. That’s the case even though the United States might not be taxing the parent’s U.S. source income at 15 percent. (However, if Ireland were to adopt a UTPR, then it could impose a top-up tax on such income.)

Further, even though some 143 countries have signed onto Pillar Two (including the United States), the GloBE rules are entirely voluntary. Certain low- or no-tax signatories (including Bermuda and the Cayman Islands) are not expected to adopt a global minimum tax, but are only agreeing to accept application of the rules applied by other signatories (but if they later decide to adopt such rules, they also agree to adopt them in a way consistent with the model rules).

Where Does U.S. Implementation Stand?

Much to the chagrin of many Republican lawmakers, the United States is an Inclusive Framework signatory. So even though it doesn’t have to adopt the GloBE rules itself, the Treasury Department (without explicit Congressional authority) signed off that the United States would “accept the application of the GloBE rules applied by other” signatories.60 Which means that, in the case of our U.S. multinational example on page 5 (with French and Cayman subsidiaries), the United States should be okay with France effectively collecting $3 million in top-up tax associated with Cayman income and another $5 million in tax associated with U.S. income as soon as the rules are fully in effect.

It turns out that the United States is not okay with this. Treasury (as reflected in the Biden Administration’s Green Book proposal61) wants the United States to (among other things) modify GILTI so that it is a compliant Pillar Two IIR and repeal the base erosion and anti-abuse tax (BEAT) and replace it with a Pillar Two compliant UTPR. And, as evidenced by the May 25 introduction of the “Defending American Jobs and Investment Act,”62 House Republicans want to punish countries that enact UTPRs63 or digital services taxes (DSTs)64 by generally increasing the rate (by between 5 and 20 percentage points) of certain income and withholding taxes on individuals, corporations and partnerships that are citizens of or domiciled in UTPR- or DST-adopting foreign countries.65

To be clear, Democrats tried (and failed) to get Pillar Two-related international tax changes passed as part of the Inflation Reduction Act of 2022 (when they controlled both the House and the Senate). Republicans, meanwhile, have continually pushed back on the OECD efforts—from both a process and a substance standpoint. One particularly harsh, but arguably fair, characterization of the result of Treasury’s involvement in OECD negotiations was given by Sen. Mike Crapo (R–Idaho), who said: “this administration handed each foreign government a robust vacuum to suck away tens of billions of dollars of our tax base—and then turn around to use those dollars to fund foreign subsidies.”66

However, there is no quick fix on the horizon. Given the politics, it is almost impossible to imagine a scenario in which the United States can realistically come into compliance with Pillar Two by the target deadlines (in 2024 for the IIR and in 2025 for the UTPR). We don’t even have legislative language for such a proposal (let alone consensus among lawmakers that such an effort is worthwhile). House Republicans’ “Defending American Jobs and Investment Act” will not pass this Congress, given Democrats’ control of the Senate—not to mention the uncertainty associated with the 2024 election (which could completely shake up political control of Congress and result in a new direction for Treasury depending on who wins the presidential election). Prognosticators are betting that the Pillar Two disagreement will most likely get roped into negotiations concerning the so-called 2025 Tax Cliff—which is when some $350 billion per year in individual and estate tax cuts from the 2017 Tax Cuts and Jobs Act are set to expire. Complicating the politics further, the Joint Committee on Taxation just issued a report on the potential effects of Pillar Two on U.S. federal tax receipts showing that there’s a good chance the United States is going to lose out on tax revenue no matter what happens.67

Which brings us back to the initial point of this report. Denial is futile.

For many U.S. multinationals, the real pain from Pillar Two potentially won’t be felt until 2025 (when UTPRs go into effect, assuming—among other things—Treasury confirms that the QDMTT is creditable in the United States).68 In that case, maybe that will buy Congress enough time to either build the consensus necessary to implement Pillar Two, or—if you agree with Republicans—convince adopting countries to reverse course on the OECD plan.

That being said, the brakes on this train may not be functional. In a May 12, 2023 letter to the editor of a prominent tax publication, a former senior international tax counsel for General Electric Co. who served in the U.S. Treasury Office of International Tax Counsel and a former Treasury Deputy Assistant Secretary for International Tax Affairs pleaded with multinationals to get off the sidelines and lobby Congress now to get on board with Pillar Two so as to avoid the inevitable train wreck on the horizon. They wrote: “Waiting is fatal. Companies need to act now. In 2025, when pillar 2 is implemented, blame for the U.S. failure to align with the global norms will rest on the taxpayers who remained silent.”69

One or more authors may have positions in stocks referred to in this article. Akin may represent individuals or entities that may have positions in stocks referred to in this article.

Akin Gump Strauss Hauer & Feld LLP has a full tax team closely following developments in this area. Please feel free to contact any of them with any questions.

1 Organisation for Economic Co‐operation and Development (OECD). For our prior coverage, see “More than 130 Countries Reach Consensus on 15% Minimum Tax and New User-Focused Taxing Right—What Are the Implications?” (July 14, 2021).

2 One such adjustment would correct for accelerated depreciation, so that it should not count against a taxpayer under GloBE.

3 The substance-based carve-out is intended to exclude a fixed return for substantive activities within a jurisdiction. In an attempt to establish that the global minimum tax is targeting intangible (and presumably highly mobile) income and not income from tangible investments, the GloBE regime allows for a deduction from GloBE income equal to 5% (but is higher during the initial transition period) of the carrying value of eligible tangible assets in the country plus eligible payroll costs in the country.

4 Note that implementing a global minimum tax is different from agreeing to be part of the OECD/G20 Inclusive Framework on BEPS (base erosion and profit shifting). As of June 9, 2023, there were 143 countries and jurisdictions (including the United States) that had signed onto the framework: https://www.oecd.org/tax/beps/inclusive-framework-on-beps-composition.pdf.

5 The accounting standards that govern U.S.-based companies are the Generally Accepted Accounting Principles (GAAP, which rules are issued by the Financial Accounting Standards Board or FASB), whereas non-U.S. firms follow the International Financial Reporting Standards (IFRS, which rules are issued by the International Accounting Standards Board or IASB).

6 Companies will have to disclose their reliance on the exception beginning as early as June 30, 2023.

7 Specifically, the extent to which the top-up tax might impact deferred taxes under IAS 12 Income Taxes.

8 As a reminder, ETR for GAAP or IFRS purposes is not the same as ETR for GloBE purposes. Because ETR for GloBE purposes is calculated using a group’s consolidated financial statements as a starting point (with adjustments for various items, including timing differences), firms that may not think they fall below the 15-percent threshold may be in for a big surprise.

9 If information is not known or cannot be reasonably estimated.

10 Note that the GloBE rules contain safe harbors that could simplify the calculations and provide relief in certain fact patterns.

11 https://fasb.org/Page/PageContent?pageId=/meetings/pastmeetings/02-01-23.html&bcpath=tff

12 For those jurisdictions accounting for at least 5% of total taxes paid.

13 https://www.fasb.org/Page/ProjectPage?metadata=fasb-Targeted%20Improvements%20to%20Income%20Tax%20Disclosures

14 https://www.iasplus.com/en/publications/global/igaap-in-focus/2023/ias-12-pillar-two

15 A note on restructuring options: A transition rule at Article 9.1.3 provides that if a multinational were to transfer IP between affiliates after Nov. 30, 2021, and before the start of a transition year, carryover basis (not stepped-up basis) rules will apply.

16 There are some disclosures. However, they are generally limited to generic statements such as: the global minimum tax “could have a material adverse effect on our aggregate tax liability and effective tax rate in the future,” company “could be adversely affected due to its income being taxed at higher effective rates, once these new rules come into force” and “prospective investors are advised to seek their own professional advice in relation to the Global Minimum Tax.”

17 https://www.pwc.com/gx/en/services/tax/pillar-two-readiness.html

18 Parent entities of multinational enterprise groups with US$850 million (€750 million) or more of revenue have been required to file country-by-country reports with U.S. or EU taxing authorities since around 2017. The EU country-by-country mandate to publicly report such information reportedly goes into effect for most multinationals in 2025.

19 https://www.sec.gov/news/speech/gensler-remarks-iac-120822

20 Jennifer Williams-Alvarez, For Tax Executives, More Disclosure on Global Liabilities Means More Headaches, Wall St. J., (May 17, 2023) (https://www.wsj.com/articles/for-tax-executives-more-disclosure-on-global-liabilities-means-more-headaches-48e06d5e); Natalie Olivo, Pressure For Corp. Tax Transparency May Just Be Beginning, Law360 (May 26, 2023) (https://www.law360.com/tax-authority/federal/articles/1681675).

21 https://www.oecd.org/newsroom/revenue-impact-of-international-tax-reform-better-than-expected.htm; For perspective, it’s projected that the United States will collect $475 billion in corporate income tax revenue for FY 2023 (https://www.cbo.gov/topics/taxes).

22 Pursuant to Article 4.2.1, covered taxes would include: “(a) Taxes recorded in the financial accounts of a Constituent Entity with respect to its income or profits or its share of the income or profits of a Constituent Entity in which it owns an Ownership Interest; (b) Taxes on distributed profits, deemed profit distributions, and non-business expenses imposed under an Eligible Distribution Tax System; (c) Taxes imposed in lieu of a generally applicable corporate income tax; and (d) Taxes levied by reference to retained earnings and corporate equity, including a Tax on multiple components based on income and equity.” For example, excise taxes and payroll taxes are not covered taxes.

23 Note that certain types of entities are excluded from Pillar Two altogether, including government entities, international organizations, nonprofits, pension funds and certain investment funds or real estate investment vehicles if (among other criteria) such fund/vehicle is the ultimate parent entity. Further, the IIR and UTPR cannot be directly assessed against certain investment entities, including investment funds whether or not it is the ultimate parent entity. While you would need to remove excluded entities before calculating a multinational group’s GloBE income and ETR (among other things), the excluded entities’ revenue is taken into account for purposes of scoping (for the €750 million Euros threshold).

24 The scope can be lower for the QDMTT (see Note 26). The €750 million scope threshold is lower than the scope for the CAMT, which requires a corporation’s average annual earnings to exceed $1 billion over a three-year testing period. Because of its lower threshold, it is believed that Pillar Two will impact many more U.S. multinationals than CAMT. Technically, the scope determination for the CAMT is in IRC §59 and is tied to IRC §59A average annual “adjusted financial statement income.”

25 https://wts.com/global/pillar-two

26 The scope for the QDMTT (which is essentially a 15% minimum tax on domestic entities) is different than the general Pillar Two scope in that countries are free to apply a QDMTT to whichever domestic entities they want, including small ones. Although implementation of a QDMTT is optional, because Pillar Two authorizes another country to collect the tax that an unlevied QDMTT leaves on the table via IIR or UTPR, there is little incentive for a country to not adopt a QDMTT (given that the undertaxed profits will be taxed by someone, why lose out on a future revenue stream). Notably, even though Ireland indicated in a March 2023 document that it would preserve its 12.5% corporate tax rate (which firms below the GloBE threshold will benefit from), it also indicated it is considering adopting a QDMTT (or QDTT) to preserve its taxing rights, presumably with respect to the larger groups that are within scope of the other Pillar Two rules (https://www.gov.ie/pdf/?file=https://assets.gov.ie/251777/588e3b10-231f-411e-8990-e0c42c895c11.pdf).

27 Note that in the earliest versions of Pillar Two, UTPR stood for the undertaxed payments rule. But upon the Dec. 20, 2021 issuance of the Pillar Two model rules, the undertaxed payment rule morphed into the undertaxed profits rule and became something much broader. The OECD BEPS project, which gets its authority from the G20 (Group of 20), has arguably since abandoned the full name of UTPR—whether it is undertaxed payments rule or undertaxed profits rule—and has elevated the term to non-acronym status, according to reporting by Stephanie Soong Johnston, Names of OECD Pillar 2 Charging Provisions Get Slight Makeover, Tax Notes, Jan. 31, 2022 (subscription required). For the model rules (Tax Challenges Arising from the Digitalisation of the Economy Global Anti-Base Erosion Model Rules (Pillar Two)), see https://www.oecd.org/tax/beps/tax-challenges-arising-from-the-digitalisation-of-the-economy-global-anti-base-erosion-model-rules-pillar-two.pdf.

28 The STTR could allow a source jurisdiction to impose a top-up withholding tax on the gross amount of certain passive related-party payments such as royalties that otherwise might have benefitted from preferential treaty protections. This rule was designed to protect developing countries, and it only applies if requested by the treaty partner.

29 As a reminder, GILTI—which is technically now only a 10.5% (21% with a 50% §250 deduction) minimum tax on a U.S. taxpayer’s foreign income—is calculated on a blended basis. Pillar Two does not allow for such blending. Further, for OECD purposes, the effective GILTI rate is currently treated as 13.125% (due to the 20% foreign tax credit disallowance) but will increase to 16.56% in 2026 (when the §250 deduction goes down to 37.5%). See also Note 31.

30 The 15% CAMT was added to the U.S. tax code as part of the Inflation Reduction Act (P.L. 117-169). See also Note 31.

31 See also Note 29. Although OECD technical guidance issued Feb. 2, 2023 provided that—for a limited time—GILTI and Subpart F would be considered blended CFC tax regimes for purposes of the GloBE calculations (which essentially means that some portion of GILTI tax—determined by application of a mechanical formula—may be allocated to low-tax jurisdictions, potentially reducing the amount of top-up tax imposed by Pillar Two), that relief sunsets when the GILTI rate goes up (it is generally only available for tax years that begin before 2026). This means that, for only a couple years, GILTI may help to lessen, but won’t altogether eliminate, the risk that IIRs and UTPRs pose to U.S. multinationals. Also under the OECD technical guidance, it appears that the QDMTT will apply before GILTI. So, for example, if Ireland adopts a QDMTT, then if a U.S. parent has an undertaxed Irish sub, Ireland gets first dibs at taxing that undertaxed Irish income (presumably raising the Irish sub’s GloBE ETR to at least 15%). This could foreclose the United States’ ability to deem a GILTI inclusion with respect to that income if Treasury confirms that the QDMTT is creditable in the United States, which to-date it has not (if it’s not creditable, the U.S. parent could face double taxation on the Irish income). If the United States does not allow a foreign tax credit (FTC) for the Irish QDMTT and applies GILTI, then the mechanical formula that determines to what extent GILTI is credited to low-tax jurisdictions for purposes of the GloBE rules would be negatively impacted (presenting a potential additional risk of double taxation depending on the make-up of the multinational group). According to press reports, the IRS is working on guidance (and Michael Plowgian, Treasury deputy assistant secretary for international tax affairs, has implied such a credit would be allowed). Importantly, although it remains unclear, CAMT does not appear to be treated as a blended CFC tax regime under the GloBE rules, because CAMT “takes into account a group’s domestic income,” which is excluded under the technical guidance.

32 Other credits may benefit from the equity method exclusion (the treatment of transferable credits, including green energy tax credits that are transferable under the Inflation Reduction Act, remains uncertain). https://sgp.fas.org/crs/misc/R47174.pdf

33 As long as the grant or refundable credit is paid out within four years, the OECD model rules treat the amount as additional income and not as a reduction in taxes, meaning that such payments will not have a detrimental impact on the group’s ETR. See page 65 definition of Qualified Refundable Tax Credit in the Pillar Two model rules (https://www.oecd.org/tax/beps/tax-challenges-arising-from-the-digitalisation-of-the-economy-global-anti-base-erosion-model-rules-pillar-two.pdf).

34 For example, by way of a deduction denial or some other type of tax reversal or reduction.

35 Loyens & Loeff is reporting that “some US MNEs are considering transferring their low-taxed constituent entity from underneath their (EU) holding company (HoldCo) structure to a country which has not yet adopted the Pillar Two rules. The main benefit of this seems that it buys them an additional year of time as the IIR already becomes effective as of December 31, 2023, whereas the UTPR becomes effective one year later.” (https://www.loyensloeff.com/insights/news--events/news/us-mnes-how-will-pillar-two-impact-your-business/#:~:text=Pillar%20Two%20contains%20transitional%20CbCR,relief%20from%20GloBE%20compliance%20obligations.)

36 With the exception of those imposed on undertaxed U.S. entities in a group.

37 Joint Committee on Taxation, Present Law and Economic Background Relating to Pharmaceutical Manufacturers and U.S. International Tax Policy (JCX-8-23), May 9, 2023. See also IRS Statistics of Income (SOI) Division Country-by-Country Reports Study from April 2023.

38 See also Note 31; Brian H. Jenn, Jonathan D. Lockhart, Elizabeth C. Lu, and Le Chen, OECD Administrative Guidance Addresses Key Pillar 2 Technical Issues, International Tax Journal, June 12, 2023 (https://answerconnect.cch.com/view/document/1d39607758e44052a5c078a80d67e60a).

39 Richard Rubin, Global Tax Mess Awaits U.S. Companies, and Congress Isn’t Helping, Wall St. J., June 17, 2023 (https://www.wsj.com/articles/global-tax-mess-awaits-u-s-companies-and-congress-isnt-helping-eec13f2c).

40 *Netherlands, *U.K., *Singapore, Cayman Islands, *Switzerland, *Ireland, Puerto Rico, Bermuda, China, *Japan, *Canada, Mexico, *Germany, Hong Kong, *Australia (*notes planned Pillar Two enactment). https://www.irs.gov/pub/irs-pdf/p5654.pdf

41 EU Directive 2022/2523, https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32022L2523

42 https://www.ato.gov.au/General/New-legislation/In-detail/Direct-taxes/International/Implementation-of-a-global-minimum-tax-and-a-domestic-minimum-tax/

43 https://www.gov.bm/sites/default/files/Budget-2023-2024-Statement.pdf

44 https://www.budget.canada.ca/2023/pdf/tm-mf-2023-en.pdf

45 Joint Statement: https://www.bundesfinanzministerium.de/Content/DE/Downloads/Steuern/g5-statement-global-minimum-effective-taxation.pdf

46 https://www.bundesfinanzministerium.de/Content/DE/Gesetzestexte/Gesetze_Gesetzesvorhaben/Abteilungen/Abteilung_IV/20_Legislaturperiode/2023-03-20-MinBestRL-UmsG/1-Diskussionsentwurf.pdf

47 https://www.gov.ie/pdf/?file=https://assets.gov.ie/251777/588e3b10-231f-411e-8990-e0c42c895c11.pdf

48 See France note.

49 https://globaltaxnews.ey.com/news/2023-5377-japan-enacts-2023-tax-reform-bill-including-legislation-to-implement-iir-to-align-with-oecd-beps-20-pillar-two

50 https://www.rijksoverheid.nl/documenten/kamerstukken/2023/05/31/wetsvoorstel-wet-minimumbelasting-2024-pijler-2

51 https://kpmg.com/sg/en/home/campaigns/2023/02/kpmg-singapore-budget-2023/tax-changes.html

52 https://www.pwc.com/us/en/tax-services/publications/insights/assets/pwc-korea-becomes-first-to-pass-p2-rules-in-its-dom-legislation.pdf

53 See France note.

54 https://kpmg.com/ch/en/blogs/home/posts/2023/06/public-votes-swiss-pillar-two-implementation.html; https://www.newsd.admin.ch/newsd/message/attachments/78827.pdf

55 https://publications.parliament.uk/pa/bills/cbill/58-03/0276/220276.pdf

56 Xerox’s Form 10-K filed Feb. 23, 2023: https://www.sec.gov/ix?doc=/Archives/edgar/data/108772/000177045023000011/xrx-20221231.htm.

57 Dolby’s Form 10-Q filed May 5, 2023: https://www.sec.gov/ix?doc=/Archives/edgar/data/1308547/000162828023015875/dlb-20230331.htm.

58 It starts out at 8% of tangible assets and 10% of payroll costs and is incrementally reduced over a 10-year transition period.

59 Among other areas of noncompliance, GILTI is calculated on an aggregate/blended—and not country-by-country—basis.

60 https://www.oecd.org/tax/beps/statement-on-a-two-pillar-solution-to-address-the-tax-challenges-arising-from-the-digitalisation-of-the-economy-october-2021.pdf

Recall that Pillar Two is only one part of the OECD/G20 Inclusive Framework on BEPS. The other part—Pillar One—would generally reallocate some taxing rights (which profits can be taxed by which countries) by reference to the location of a business’s users. Pillar One has never been as far along as Pillar Two, which is starting to become a problem for the United States. That’s because, pursuant to a larger OECD statement dated Oct. 8, 2021, (https://www.oecd.org/tax/beps/statement-on-a-two-pillar-solution-to-address-the-tax-challenges-arising-from-the-digitalisation-of-the-economy-october-2021.pdf) parties essentially agreed to a standstill with respect to the imposition of DSTs or similar measures while the details of Pillar One were worked out. (Pillar One was designed to get at the Facebooks, Googles and Amazons (Facebook, Inc. (NASDAQ: FB), Alphabet Inc. (NASDAQ: GOOGL) (Google) and Amazon.com, Inc. (NASDAQ: AMZN)) of the world, and the general idea is that Pillar One is preferable to unilateral DSTs that target the same types of companies.) If the Multilateral Convention (the text of which is expected be finalized in July 2023, according to Stephanie Soong, OECD Body Co-Chair Calls for Modular Pillar 1 Tax Accord Process, Tax Notes Today International, June 6, 2023 (subscription required)) expected to implement Pillar One is not in force by Dec. 31, 2023 (the expiration date of the standstill agreement), then countries including Austria, France, Italy, Spain and the United Kingdom (https://home.treasury.gov/news/press-releases/jy0419#:~:text=Under%20the%20Unilateral%20Measures%20Compromise,until%20Pillar%201%20takes%20effect.) (among others) can enforce their DSTs (and the United States can pursue retaliatory trade actions proposed under Section 301 of the Trade Act of 1974). Note that, in some cases (including the United Kingdom’s 2-percent DST), countries are already collecting DSTs from U.S. multinationals, but they essentially agreed to let those multinationals reduce their future Pillar One liability by the amount of their DST payments. However, according to press reports June 8, 2023, Treasury is concerned that the Dec. 31, 2023 deadline won’t be met and wants the standstill agreement extended “to avert a trade war among friends and keep alive a foundering global tax deal.” (Christopher Condon and Brian Platt, US Seeks to Extend Digital-Tax Freeze as Global Deal Stalls (2), Bloomberg News, June 8, 2023 (https://www.bloomberglaw.com/product/tax/bloombergtaxnews/daily-tax-report-international/BNA%2000000188-9c56-d4e2-a1cb-fede4d870000?isAlert=false).) (According to the national Audit Office, HM Revenue & Customs received an aggregate of £358 million in DST receipts for the 2021-2021 tax year from 18 multinational groups, 90% of which was incurred by only five groups. https://www.nao.org.uk/wp-content/uploads/2022/11/Investigation-into-the-digital-services-tax.pdf)

61 FY 2024 General Explanations of the Administration's Revenue Proposals (https://home.treasury.gov/system/files/131/General-Explanations-FY2024.pdf).

62 https://waysandmeans.house.gov/ways-and-means-republicans-introduce-bill-to-combat-bidens-global-tax-surrender/

63 U.S. lawmakers haven’t shown much desire so far to push back against countries enacting IIRs or QDMTTs (presumably believing it’s their sovereign right to tax what amounts to the income of CFCs—as the United States did with GILTI—and impose minimum taxes—as the United States did with CAMT).

64 For more on DSTs, see our prior report “Multi‐Billion Dollar Digital Services Tax Could Fall on Few U.S. Companies, Harming Consumers and/or Stock Prices” (Sept. 19, 2019).

65 The House Republican bill is actually much broader. It would impose additional countermeasures that would prohibit the Federal Government from procuring goods or services from individuals or entities that are either citizens of or domiciled in countries that have in place an “extraterritorial” or “discriminatory” tax (designed to target UTPRs and DSTs) and would limit the ability of the United States to enter into a bilateral tax treaty or a free trade agreement with such countries.

66 Global Minimum Tax Deal Ropes US Into Subsidy Free-for-All, Bloomberg Tax, May 16, 2023 (https://www.bloomberglaw.com/product/tax/bloombergtaxnews/tax-insights-and-commentary/XKI4KVK000000).

67 Joint Committee on Taxation, Possible Effects of Adopting the OECD’s Pillar Two Both Worldwide and in the United States (June 2023). In one scenario, if the rest of the world enacts Pillar Two in 2025 and the United States does not, then U.S. federal tax receipts could decrease by an estimated $122 billion over a 10-year period (assuming a small decrease in profit shifting by U.S. multinationals from low-tax jurisdictions into the United States). On the other hand, if both the United States and the rest of the world enact Pillar Two in 2025, then U.S. federal tax receipts are still estimated to decrease by some $57 billion over a 10-year period (assuming a small increase in profit shifting by U.S. multinationals into the United States), presumably because of increased allowable foreign tax credits (for example, on QDMTTs).

68 For a more nuanced summary, see pages 6 and 7 beginning with “The upshot is. . .”

69 Peter A. Barnes and Stephen E. Shay, No Time for Waiting, Tax Notes, May 22, 2023 (subscription required).

Key Contacts