How Many ATBs Does Liberty Media Have?

By: Stuart E. Leblang, Michael J. Kliegman and Amy S. Elliott

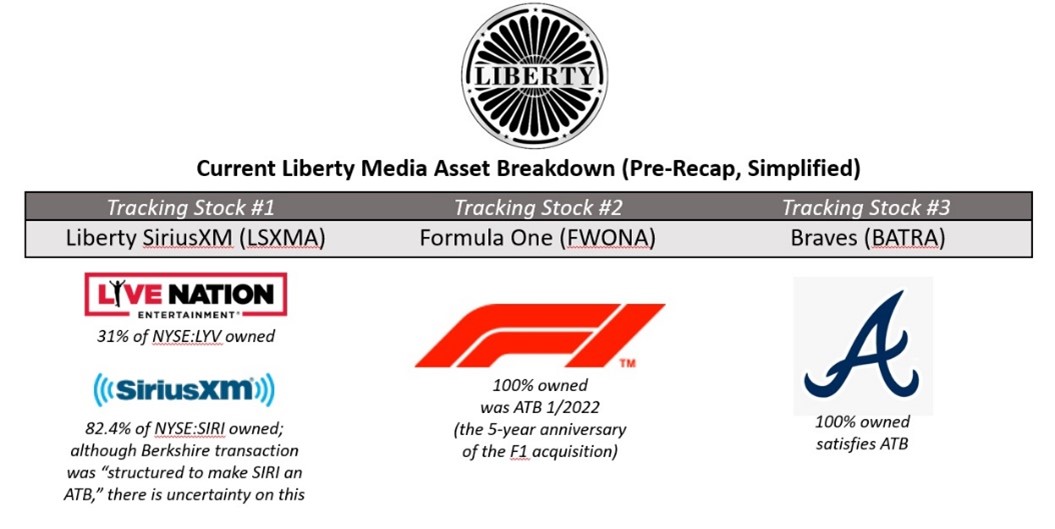

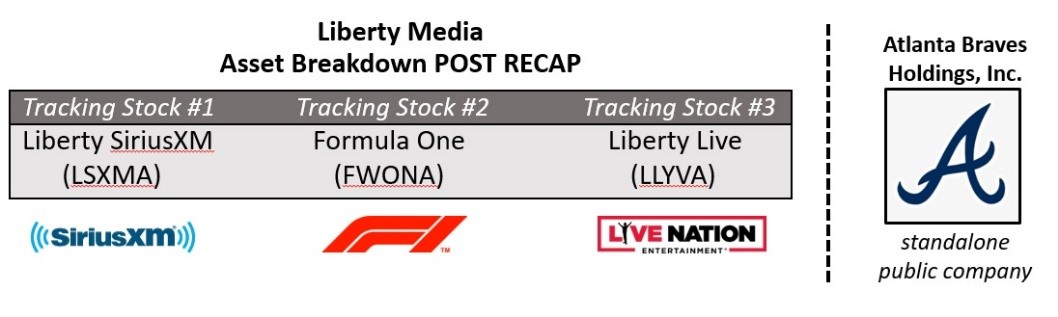

As we discussed in our December 22, 2022 report, Liberty Media Corporation (Liberty Media) plans to split off the assets and liabilities associated with the Atlanta Braves Major League Baseball team into a standalone, newly formed public company (Atlanta Braves Holdings, Inc., also known as Braves Splitco), doing away with the Braves tracking stock (NASDAQ: BATRA).1 Details about the transaction are provided in Braves Splitco’s recently filed amended Form S-42, including the distribution of shares in the new Braves Splitco to holders of Liberty Formula One tracking stock (NASDAQ: FWONA), taking into account inclusion of a portion of the Braves group within the Formula One group.

Braves Splitco also filed a disclosure on April 6 regarding its requested ruling from the Internal Revenue Service (IRS) with respect to the split-off transaction.3 The disclosure states that “the requested Ruling was premised on, among other things, that Liberty Media’s ownership and operation of the business conducted through its subsidiary, Sirius XM Holdings Inc. (the ‘SiriusXM business’), would satisfy the active trade or business requirement under Section 355 of the Code (the ‘ATB Requirement’).”4 The disclosure further states: “By letter dated March 15, 2023, the IRS informed Liberty Media that, in the general interest of sound tax administration, the IRS was declining to provide the requested ruling until certain issues were resolved under its open regulation project addressing certain requirements under Section 355 of the Code, including the ATB Requirement.”

The transaction will proceed as planned, because the company’s tax counsel confirmed that it will issue a “will” level opinion as to the transaction’s qualification under Section 355 (and because receipt of the IRS ruling was a waivable condition to completion of the split-off).

We are not surprised that the IRS was unable to conclude that Liberty Media’s ownership of more than 80 percent of Sirius XM Holdings Inc. (NASDAQ: SIRI) (SiriusXM) satisfied the ATB requirement. As we discussed in a November 10, 2021 report (copy attached),5 a then-recent tax-free exchange by Berkshire Hathaway of a relatively small amount of SiriusXM stock for Liberty SiriusXM tracking stock (NASDAQ: LXSMA) (Liberty SiriusXM) that increased Liberty Media’s voting interest in SiriusXM from a little less than 80 percent to a little more than 80 percent (i.e., “control” for purposes of the reorganization provisions) could arguably allow it to satisfy the requirements for an ATB.6 As we explained in that report, although Liberty Media CEO Greg Maffei stated on a call that they intended the transaction to “make an ATB,” the tax law was not clear as to whether this was the case (because even though the 80-percent threshold was achieved in a tax-free transaction, much of its ownership was acquired in taxable transactions7). Apparently, the IRS regards the question as unclear as well.

What we find interesting about Liberty Media’s disclosure about the IRS ruling8 is that it asked the IRS to determine ATB status of the SiriusXM holding despite the fact that, aside from the Braves business being split off, it had a clean five-year ATB in Formula One9 as of January 2022.10 The April 6 disclosure states that “ subsequent to receiving notice of the IRS’s decision with respect to the ruling request, Liberty Media confirmed with its tax counsel, Skadden Arps Slate Meagher & Flom, LLP (‘Skadden’), that the decision by the IRS not to provide a ruling at this time did not affect Skadden’s view that, under current law, and subject to certain factual representations and assumptions, the ATB Requirement will be satisfied with respect to Liberty Media in connection with the Split-Off Transactions by Liberty Media’s ownership and operation of the SiriusXM business.” The next sentence states that “Skadden further confirmed to Liberty Media that . . . the IRS’s decision would not affect Skadden’s ability to render an opinion . . . to the effect that . . . the Split-Off Transactions will qualify as a tax-free transaction under Section 355 . . . .”

The flow of these two sentences connotes that Skadden’s anticipated “will” opinion on the split-off will be based on its determination at that high level of comfort that Liberty Media’s ownership of stock in SiriusXM will satisfy the ATB requirements. Under the circumstances, it would surprise us if Skadden were to base its opinion solely on that technically shaky issue when it seems to be the case that Liberty Media has in its Formula One business a much stronger position on ATB. In this regard, we would expect Skadden to continue to embrace a position with respect to SiriusXM that the IRS may view as unclear, while relying on Formula One as its fallback ATB to support the “will” level opinion.

If Skadden is right and Liberty Media’s SiriusXM stake currently satisfies the ATB requirement, then (assuming it’s comfortable relying solely on Skadden’s opinion on that point despite the IRS’s apparent unwillingness to rule favorably on that issue) Liberty Media could split off its SiriusXM stake into a newly formed, separate public company at any time without fear of triggering violating the ATB requirement.

However, if Liberty Media’s SiriusXM stake won’t clearly become an ATB until November 2026 (the five-year anniversary of the Berkshire Hathaway transaction), must they wait until then to effect a tax-free separation of SiriusXM from its other holdings? We think there is a path to doing this sooner, via a merger of Liberty Media with and into SiriusXM, followed by a split-off (by SiriusXM, rather than Liberty Media) of New Liberty Media (so-called New Liberty Media Splitco) with only two tracking stocks (one for its Live Nation11 holding and one for its Formula One holding). Liberty SiriusXM tracking stock holders would walk away from the transaction with stock in SiriusXM itself.

This approach is premised on the fact that SiriusXM itself unquestionably has a five-year ATB, but this is only useful if SiriusXM is the distributing corporation in the Section 355 split-off. The steps, all previously agreed upon and binding on the parties would be:

- Liberty Media merges with and into SiriusXM. In the merger:

- Holders of Liberty SiriusXM exchange those shares for shares of SiriusXM common stock at an agreed exchange ratio.

- Holders of Liberty Formula One exchange those shares for shares of a newly authorized class of SiriusXM stock (Sirius XM Liberty Formula One).

- Holders of Liberty Live exchange those shares for shares of a newly authorized class of Sirius XM stock (Sirius XM Liberty Live).

- Immediately after the merger, shares of Sirius XM Liberty Formula One and Sirius XM Liberty Live are redeemed in exchange for shares of New Liberty Media Splitco. Sirius XM Liberty Formula One shares are exchanged for New Liberty Media Splitco Formula One stock, and Sirius XM Liberty Live shares are exchanged for New Liberty Media Splitco Live stock.

It would be simpler for Liberty Media to do the split-off before merging with Sirius XM, but we think it may be technically necessary that, in form, Sirius XM (rather than Liberty Media) be the corporation engaging in the tax-free Section 355 distribution. Technically (and these are rather technical rules), Sirius XM as the distributing corporation will be engaged in an ATB after the split-off that it has actively carried on for five years, and New Liberty Media Splitco will have a five-year active business in Formula One that has been actively carried on for five years and was only acquired by Sirius XM in a transaction in which no gain or loss was recognized.12

Any transaction in which there is a full separation of Liberty Media’s Sirius XM holding from Formula One and Live Nation will require the active participation of Sirius XM, and would likely involve a merger as a result of which the only equity instrument through which to own an interest in the Sirius XM business would be Sirius XM common stock.

Liberty Media hasn’t been shy about disclosing its focus on ATBs in recent years. As CEO Greg Maffei stated in 2021, “we always like having ATBs. You can’t have enough of them.”13 We suspect the reason Liberty Media sought a ruling from the IRS with SIRI as the ATB rather than Formula One is so that Liberty Media could get the IRS’s blessing on the Siri ATB, which the company could then use in case it decides to effect a split of the SIRI stake prior to 2026. Only time will tell what Liberty Media decides to do next.

One or more authors may have positions in stocks referred to in this article. Akin may represent individuals or entities that may have positions in stocks referred to in this article.

Akin Gump Strauss Hauer & Feld LLP has a full tax team closely following developments in this area. Please feel free to contact any of them with any questions.

1 “Liberty Media to Split Off Atlanta Braves Creating Liberty Live Tracking Stock” (Dec. 22, 2022).

2 Atlanta Braves Holdings, Inc. Amended Form S-4 filed April 6, 2023 (https://www.libertymedia.com/investors/financial-information/sec-filings/content/0001104659-23-042265/0001104659-23-042265.pdf).

3 Atlanta Braves Holdings, Inc. Form 425 filed April 6, 2023 (https://www.libertymedia.com/investors/financial-information/sec-filings/content/0001104659-23-042262/0001104659-23-042262.pdf).

4 See Internal Revenue Code (IRC) §355(b), which requires that Spinco (or Splitco) and Remainco each be engaged in an active trade or business that has been continuously carried on for at least five years (and was not acquired during the five-year period in a taxable transaction).

5 “Tax Considerations of Berkshire Hathaway’s Exchange of SiriusXM Stock for Liberty SiriusXM Tracking Stock” (Nov. 21, 2021).

6 Liberty Media beneficially owned, directly and indirectly, about 79% of Sirius XM Holdings Inc. stock as of Sept. 30, 2021, but the Berkshire Hathaway transaction caused its ownership to increase to about 80.2% as of Nov. 1, 2021. Note that as of Jan. 31, 2023, Liberty Media’s ownership of Sirius XM stock was at about 82.4% (as a result of additional stock buybacks by SiriusXM).

7 After purchasing an additional 50 million shares of SiriusXM stock, Liberty Media acquired a controlling interest in SiriusXM on January 18, 2013. Over the years, Liberty Media’s percentage ownership in SiriusXM has increased as (among other factors) SiriusXM has repurchased its shares.

8 It is somewhat baffling why, if we are correct in assuming that the IRS informed Liberty Media that the Service was not comfortable issuing a ruling on the SiriusXM ATB question, the company and its tax advisors did not instead ask the IRS to rule favorably on §355 with reference to the Formula One ATB (which involves more straightforward facts). The IRS noted in its March 15 letter that it was declining to rule in part due to to its open §355 regulation project addressing, among other things, the ATB requirement. Although the project was added to the IRS Priority Guidance Plan Oct. 8, 2019, the IRS has since issued rulings that a distribution satisfies the ATB requirement in spite of the open project.

9 Formula 1 is a wholly-owned consolidated subsidiary of Liberty Media.

10 Because Liberty Media acquired Formula 1 on Jan. 23, 2017. See slide 9 of the 2020 Liberty Investor Day presentation, which states: “Braves are currently an ATB…F1 will be an ATB in January 2022.” (https://d1io3yog0oux5.cloudfront.net/_a69c4133fc07485acdc43ac2872c4ebd/libertymedia/db/1987/19307/pdf/Liberty-Media-Corp-Thursday-November-19-2020.pdf).

11 As of Jan. 31, 2023, Liberty Media’s ownership of Live Nation Entertainment, Inc. (NYSE: LYV) was at about 31%.

12 See IRC §355(b)(2)(C).

13 Transcript of Liberty Media Q3 2021 earnings call Nov. 4, 2021 provided by Seeking Alpha (https://seekingalpha.com/article/4466282-formula-one-group-fwona-ceo-stefano-domenicali-on-q2-2021-results-earnings-call-transcript).

Key Contacts