Macquarie Infrastructure Corporation to Restructure Under Partnership Parent to Facilitate Liquidation

By Stuart E. Leblang, Michael J. Kliegman, and Amy S. Elliott

On February 17, Macquarie Infrastructure Corporation (NYSE: MIC) (MIC) announced plans to reorganize under a publicly traded partnership—Macquarie Infrastructure Holdings, LLC (Holdings LLC)—in order to minimize the amount of tax MIC would have to pay on the gain from the sale of its businesses.[1]

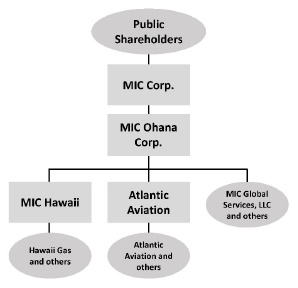

MIC owns and operates two businesses—Atlantic Aviation (a provider of fuel, terminal, aircraft hangaring and other services at 69 U.S. airports) and MIC Hawaii (which processes and distributes gas and provides related services in Hawaii)—both of which suffered from decreased activity early in 2020 due to the COVID-19 pandemic.[2]At the end of October 2019, MIC announced that it had decided to “actively pursue strategic alternatives including a sale of the Company or its operating businesses as a means of unlocking value for shareholders.”[3]

Atlantic Aviation is the larger of MIC’s two businesses and is expected to generate more than six times the earnings before interest, depreciation and amortization (EBITDA) in 2021 as compared to MIC Hawaii.[4]According to Christopher Frost, MIC’s Chief Executive Officer, the planned restructuring will enable MIC “to sell Atlantic Aviation prior to selling MIC Hawaii without incurring corporate capital gains tax.”[5]

Planning for an Efficient Liquidation

Ordinarily, when a company decides to liquidate by selling off its business assets and distributing the proceeds out to shareholders, the sales are often taxable at the corporate-level, reducing the amount of proceeds that end up in the hands of shareholders.[6]MIC has decided the more efficient path would be to sell the smaller MIC Hawaii and avoid paying any tax on the larger disposition (the sale of Atlantic Aviation) by structuring it as a sale of MIC stock (rather than as an asset sale). This would most naturally involve ordering the two transactions such that the MIC Hawaii sale would precede the Atlantic Aviation sale via a sale of MIC. However, due to the expected length of the process of obtaining regulatory approvals in Hawaii (a process that could take twelve months or longer),[7]an MIC Hawaii transaction cannot occur very soon, while an Atlantic Aviation disposition can proceed more expeditiously. Hence, the proposed restructuring, which will be subject to a shareholder vote at a special meeting, the date of which has yet to be determined.

There are three primary components of MIC’s plan:[8]

Step One: The Merger, Resulting in a New Partnership Parent

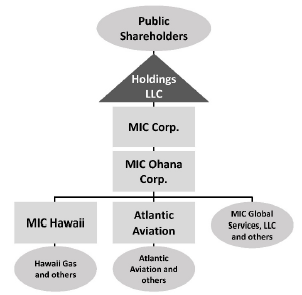

First, MIC will form a wholly owned limited liability company (LLC) subsidiary by the name of Macquarie Infrastructure Holdings, LLC (Holdings LLC), which is intended to be taxed as a partnership. Holdings LLC will then form a wholly owned corporate subsidiary by the name of Plum Merger Sub, Inc. (Merger Sub). Merger Sub will then merge with and into MIC, with MIC surviving as a wholly owned subsidiary of Holdings LLC (MIC will be delisted and Holdings LLC will become the publicly traded entity). For tax purposes, the merger is expected to be treated as a tax-free contribution of MIC stock by MIC’s shareholders to Holdings LLC in exchange for Holdings LLC units (on a one-for-one basis) under Internal Revenue Code (IRC) section 721.

|

|

|---|

Step Two: The Hawaii Distribution

Then, MIC Ohana Corporation, a direct wholly-owned subsidiary of MIC, will distribute to MIC the equity of MIC Hawaii Holdings, LLC (which holds the MIC Hawaii business), and MIC will in turn distribute the MIC Hawaii equity to Holdings LLC. While this distribution will precede the ultimate sale of the MIC Hawaii business (by way of a sale of Holdings LLC), that could take some time.[9]

The distribution will result in taxable gain to MIC to the extent that the fair market value of the distributed interest in MIC Hawaii exceeds MIC Ohana Corporation’s adjusted tax basis in the same. To the shareholders (as partners in Holdings LLC), the distribution will be taxable as a dividend to the extent of MIC’s current and accumulated earnings and profits (allocated pro rata among unitholders). Any excess will be treated first as non-taxable return of capital up to Holdings LLC’s tax basis in its MIC stock (which is a carryover of the shareholders’ tax basis from Step One, and then any remainder will be taxed as capital gain to the unitholder. Of note, no cash distribution will be made to help unitholders cover the cost of the tax hit associated with the Hawaii Distribution.

Step Three: The Disposition of MIC

Steps One and Two will not occur until after MIC has executed a definitive agreement to sell its Atlantic Aviation business, and such sale will be closed following Step Three. Once MIC Hawaii is removed from the MIC corporate box, which now only contains Atlantic Aviation, that larger business can be sold as a sale of MIC stock in a tax-efficient manner. Taxable gain from the sale of MIC stock will be allocated by Holdings LLC to the partners (presumptively, but not necessarily, the former MIC shareholders) and such gain will be taxable to them.

Issues Raised by the Transaction

There are unquestionably a number of unusual aspects to the series of transactions planned by MIC. But at its core, this involves the sort of blocking and tackling that much M&A tax planning involves. With two businesses to sell, run the numbers and determine which would result in materially greater tax cost to the corporation (i.e., larger gain), have the corporation sell the other business and then arrange a sale by the shareholders of the stock of the corporation. Here, the high tax cost business is Atlantic Aviation and the lower tax cost business is MIC Hawaii. But there is a timing problem: Atlantic Aviation is ripe for sale while, due to regulatory delays, MIC Hawaii is not.

The culminating event will be the eventual sale of the MIC Hawaii business. We would have thought the expeditious approach would be for Holdings LLC to sell MIC Hawaii to the eventual buyer. However, the only indications of how this transaction would be structured—the February 17 press release and related earnings call—state that “MIC Hawaii would be sold via a sale of [Holdings LLC].”[10]The reason we are a little surprised by this is that, while Holdings LLC could execute the sale of MIC Hawaii via a purchase agreement with a buyer, the sale of a publicly held entity such as Holdings LLC would presumably require a merger agreement and corresponding proxy statement and shareholder approval. In fact, the LLC Agreement requires a vote of the investors even if Holdings LLC were to sell MIC Hawaii (which would be substantially all of its assets).[11]Given the plan is in place to engage in such a sale, one might have thought that this could have been pre-wired from a governance standpoint, but that is not the route they chose.

The plan is essentially for MIC to engage in a taxable spin-off of MIC Hawaii to the shareholders, and then sell Atlantic Aviation via sale of MIC stock. So why are they not doing exactly that? The shareholders could vote on a merger plan that would bring about the sale of MIC and distribution of MIC Hawaii and the sale proceeds to the shareholders, leaving MIC Hawaii as the ongoing public company waiting to be sold. The company does not answer that question.

Subject to caveats by the company about not running afoul of the publicly traded partnership (PTP) tax rules,[12]Holdings LLC will be a pass-through vehicle for tax purposes, and though it will be active in overseeing the process of selling MIC and MIC Hawaii, one might compare its role to that of a liquidating trust. Investors should be aware of the differences between holding a share of common stock and holding a unit in a publicly traded partnership.[13]

One question we have from reviewing the public information about the transaction is whether MIC Hawaii Holdings, LLC, the entity conducting the Hawaii business, is a pass-through or corporate entity for U.S. tax purposes.[14]The tax disclosure in the Form S-4 discusses the possibility that Holdings LLC could potentially be treated as a corporation for U.S. tax purposes if its income does not meet the requirements of passive-type income to retain partnership status as a publicly traded entity.[15]The expressed concern implies that Holdings LLC’s only asset (after selling MIC), the equity of MIC Hawaii, might be a pass-through entity directly engaged in business in Hawaii. Much of the discussion of tax considerations facing holders of Holdings LLC units indicates that it will own business assets rather than shares of an operating corporate subsidiary. However, we also see evidence in the Preliminary Registration Statement indicating MIC Hawaii is a corporate entity, which has bearing on the tax treatment to U.S. and foreign investors.[16]

Impact on Foreign Investors

The merger resulting in the exchange of MIC stock for Holdings LLC units should not be taxable to U.S. or foreign investors. However, the subsequent step in which MIC distributes the equity of MIC Hawaii to Holdings LLC will be a dividend subject to withholding tax of 30 percent on the value of the MIC Hawaii interest, capped at the amount of MIC’s earnings and profits. We think this problem can be easily avoided by the company, without adversely affecting other interests. If MIC distributes MIC Hawaii to Holdings LLC not as a state law dividend, but in exchange for the surrender of shares in MIC, the distribution will fall within the redemption rules of IRC section 302. Standing alone, a redemption of shares from the sole shareholder does not reduce its percentage interest in the corporation, and so, would still be treated generally as a dividend. However, under the well-established Zenz doctrine,[17]when such a redemption occurs immediately prior to a prearranged sale of the stock of the distributing corporation, the redemption qualifies as a complete termination of interest resulting in sale, rather than dividend, treatment.[18](See discussion below regarding FIRPTA considerations.)

There is discussion in the Form S-4 about the applicability of the Foreign Investment in Real Property Tax Act of 1980 (FIRPTA) to the subsequent transactions. Specifically, the company states that after distributing interests in MIC Hawaii, MIC will likely be treated as a U.S. real property holding corporation (USRPHC) such that gain on the disposition of shares in MIC will be subject to taxation under FIRPTA. This triggers a general U.S. tax return filing requirement for foreign investors in Holdings LLC. Holders of 5 percent or less of a publicly traded corporation’s stock during the preceding five-year period are generally exempt from the FIRPTA tax.[19]Pursuant to regulations, interests in a publicly traded partnership also qualify for this exemption, such that a disposition of an interest in a publicly traded partnership that owns FIRPTA property by a qualifying 5 percent or less holder is not taxable under the FIRPTA rules.[20]However, as structured, the FIRPTA disposition event will be the sale by Holdings LLC, a publicly traded partnership, of 100 percent of the stock of MIC, a non-publicly traded USRPHC, with the gain passing through to investors under the partnership rules. The regulations do not explicitly extend the “publicly traded” exemption to this situation. The Form S-4 notes that foreign investors that owned 5 percent of less of pre-merger MIC “might be eligible for an exception.”[21]The company may be referring to an argument based on equitable principles, or “substance over form” (e.g., the merger, Hawaii distribution and sale of MIC were pursuant to an integrated plan, so the publicly traded exemption should apply).

The way the company refers to post-distribution MIC likely being a USRPHC and no mention about pre-merger MIC or stand-alone MIC Hawaii implies that they do not think either (pre- merger MIC or stand-alone MIC Hawaii) presents a FIRPTA concern. If this is the case, then converting the distribution of MIC Hawaii from a dividend to a redemption would not present a FIRPTA problem for foreign investors. Following the disposition of MIC, MIC Hawaii (assuming it is a corporation for tax purposes) is presumably not likely to be a USRPHC. From this standpoint, and the fact that the company states that it does not expect there to be (non-FIRPTA) effectively-connected income giving rise to U.S. taxation to foreign investors, it may be that foreign investors can hold interests in Holdings LLC and participate in the disposition of MIC Hawaii without U.S. taxation.

[1] Press Release, MIC, MIC Reports Fourth Quarter and Full Year 2020 Financial and Operational Results, Announces Corporate Reorganization as a Limited Liability Company (Feb. 17. 2021) (https://www.sec.gov/Archives/edgar/data/1289790/000162828021002303/exhibit991_20201231.htm).

[2] Id.

[3] Press Release, MIC, Macquarie Infrastructure Corporation Announces Intention to Pursue Strategic Alternatives (Oct. 31, 2019) (https://www.sec.gov/Archives/edgar/data/1289790/000115752319002147/a52120703ex99_1.htm).

[4] Supra, note 1.

[5] Excerpts from the Transcript of Macquarie Infrastructure Corporation Earnings Call held on February 17, 2021 (https://www.sec.gov/Archives/edgar/data/1289790/000110465921024864/tm217050d1_425.htm).

[6] Although any distributions that the company makes out to its shareholders following the adoption of a plan of liquidation would be considered to be made in exchange for the shareholders’ stock under Internal Revenue Code (IRC) §331 and would avoid dividend treatment.

[7] The Holdings LLC preliminary Form S-4 dated Feb. 17, 2021 (Preliminary Registration Statement) (https://www.sec.gov/Archives/edgar/data/1845290/000110465921024660/tm216862-1_s4.htm) states: “under our current structure, the uncertainty and unknown length of time associated with the [Hawaii Public Utilities Commission] approval for a sale of MIC Hawaii could result in a significant delay to achieve a tax-efficient sale of our Atlantic Aviation business.” The 12 months is from this Feb. 17, 2021 transcript excerpt: https://www.sec.gov/Archives/edgar/data/1289790/000110465921024864/tm217050d1_425.htm.

[8] Details of which can be found in the Preliminary Registration Statement.

[9] Completion of the sale of the LLC would be subject to the Hawaii Public Utilities Commission change of control approval process (https://www.sec.gov/Archives/edgar/data/1845290/000110465921024660/tm216862-1_s4.htm).

[10] The related earnings call similarly states that: “The last step in the process would be the sale of the LLC then owning only MIC Hawaii. Completion of the sale of the LLC would be subject to the Commission’s change of control approval process I mentioned earlier” (https://www.sec.gov/Archives/edgar/data/1289790/000110465921024864/tm217050d1_425.htm).

[11] According to the Preliminary Registration Statement, “[t]he LLC Agreement provides that Holdings LLC will not merge or consolidate with any other entity or sell, lease or exchange all or substantially all of its property and assets, unless a majority of the board of directors and a majority of the unitholders holding the voting power of the issued and outstanding common units of Holdings LLC entitled to vote thereon approve the transaction.”

[12] It is expected that 90 percent or more of Holdings LLC’s gross income will constitute qualifying income under §7704(d) such that, even though the partnership is publicly traded, it will not incur corporate-level tax. However, such expectation is not certain, as explained in the Form S-4: “[G]iven the highly complex nature of the rules governing partnerships, the ongoing importance of factual determinations, and the possibility of future changes in Holdings LLC’s circumstances, no assurance can be given by Holdings LLC that it will so qualify for any particular year. Holdings LLC’s taxation as a partnership will depend on its ability to meet, on a continuing basis, through actual operating results, the ‘qualifying income exception’ . . . No assurance can be given that the actual results of Holdings LLC’s operations for any taxable year will satisfy the qualifying income exception.”

[13] For example, instead of receiving a Form 1099-DIV, the investor will receive a Schedule K-1. Further, certain investors do not invest in pass-through entities. Interests in an LLC are ineligible for inclusion on any S&P Dow Jones U.S. index and any Russell index, and MIC disclosed that while its common stock is currently included in certain stock indexes and their respective tracking funds, “[i]f the merger is completed, the common units of Holdings LLC will not qualify for inclusion in, and may be removed from, one or more of such indexes . . . [which] could adversely impact the market price of the common units” (https://www.sec.gov/Archives/edgar/data/1845290/000110465921024660/tm216862-1_s4.htm).

[14] Under the check-the-box regulations, a limited liability company may be treated as a pass-through entity (disregarded with only one owner, a partnership with multiple owners) or as a corporation for tax purposes if a proper election is filed (Treas. Reg. §301.7701-3).

[15] See IRC §7704(d).

[16] For example, on page 79 of the Preliminary Registration Statement, the company states that “Holdings LLC’s method of operation will not result in Holdings LLC generating income treated as effectively connected with the conduct of a U.S. trade or business. . . .” Also, on page 80, in the discussion of the FIRPTA rules (discussed below in the text) refers to the possibility that MIC Hawaii might constitute a U.S. real property holding corporation (USRPHC), which is only possible if it is a corporation for U.S. tax purposes.

[17] See Zenz v. Quinlivan, 213 F.2d 914 (6th Cir. 1954); Rev. Rul. 75-447, 1975-2 C.B. 113.

[18] IRC §302(b)(3).

[19] IRC §897(c)(3).

[20] Treas. Reg. §1.897-1(c)(2)(iv).

[21] The Form S-4 states: “While it is not free from doubt, it is likely that, following the reorganization, MIC Corp. will be treated as a USRPHC. Accordingly, in such case, a sale of MIC Corp. by Holdings LLC generally would cause each non-U.S. holder to be subject to U.S. federal income tax pursuant to FIRPTA on such holder’s allocable share of any gain realized from such sale and subject to the tax return filing requirements regarding effectively connected income discussed above, unless an applicable exception applied. Certain non-US holders that received their Holdings LLC common units in the merger and that owned, actually or constructively, 5% or less of the MIC Corp. common stock throughout the shorter of the five-year period ending on the date of the merger or the non-U.S. holder’s holding period for the MIC Corp. common stock might be eligible for an exception. Holders should consult their own tax advisors regarding the availability of and their eligibility for an applicable exception.”

Key Contacts